Defense Firms Angle for Eastern Europe

One of the more dissonant aspects of NATO field exercises is, three decades after the fall of the Berlin Wall, the continued presence of Warsaw Pact weapons and equipment: Soviet-made T-series tanks, MiG fighters, Mi-17 helicopters, BM-21 rocket artillery, and more.

Like their western counterparts on the continent, Central and Eastern Europe (CEE) states have repeatedly delayed needed recapitalization as defense needs gave way to domestic imperatives. But times – and threat assessments – are changing.

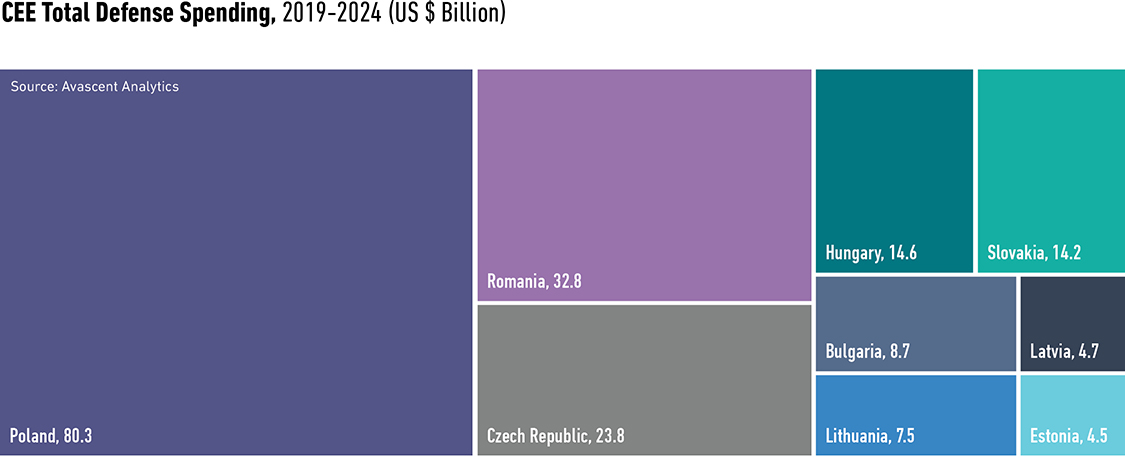

By our analysis, cumulative CEE defense spending will be nearly $200 billion over the next five years, growing by nearly five percent per year. More than a quarter of that total, some $53 billion, will be spent on defense hardware procurement.

This represents a rare opportunity for Western defense firms – European and American – to seize a first-mover advantage. However, US companies must find new ways to credibly differentiate themselves from European competitors that may offer more financial and industrial incentives (and fewer regulatory hassles) in the long run.

Currently, US companies are well positioned for success as more aggressive US government advocacy has led to recent CEE customer wins for Black Hawk helicopters (Latvia, Poland, Slovakia), F-16 fighters (Bulgaria, Slovakia), HIMARS (Poland, Romania), JLTV (Lithuania), and Patriot AMD systems (Poland, Romania).

billion over the next five years, growing by nearly 5%

per year. More than a quarter of that total, some

$53 billion, will be spent on defense hardware

procurement."

The US effort to steer CEE weapons-buying decisions picked up further momentum last year with the State Department-led European Recapitalization Incentive Program (ERIP), which provided $190 million in financing assistance to five Balkan countries (along with Slovakia) to replace ex-Soviet and Yugoslav-made equipment.

Even as ERIP expands, American companies will still have plenty of obstacles ahead. Historically, the limited new weapons procurement in most CEE countries included minimal offset or local industrialization requirements.

Going forward, reporting suggests that CEE countries, even as small as Croatia or Slovenia, will demand some form of local industrial participation and technology cooperation to develop their indigenous capabilities. This puts American firms at a disadvantage given the US government’s still-stringent technology transfer regime.

Western European companies will differentiate themselves by proposing generous technology and work-sharing transfers, integrating local defense companies into their supply chains, and setting up a pan-European Defense Industrial Base.

The European Defense Fund (EDF) will fuel this by providing up to €13 billion over the next eight years to cultivate and secure these local ties. By financing collaborative R&D projects, prototype development, and disruptive, higher-risk defense innovation, the EDF will entrench Western European companies in CEE defense establishments over the medium to long term.

Yet, from the perspective of vulnerable members on NATO’s eastern flank, only the US has the political power and defense capabilities to counter Russian meddling and aggression.

Given the ambivalence of Western European powers about confronting Russia, and the appearance of oft-fluctuating US commitment to NATO, CEE nations may see buying American not only as a means to get best-in-class (but more costly) weapons, but also as a binding mechanism to enhance US political and military commitment.

This dynamic was most vividly illustrated with Poland as it announced its intention to pursue the F-35, a platform historically out of Poland’s “price range.” The purchase was also one of three major cornerstones for ensuring US investment in Polish security. The others were Poland’s procurement of Patriot AMD systems and its agreement to – and its offer to fund – enduring US basing in-country.

However, Poland will still expect significant local industrial benefit as part of any arms transaction, as defense acquisitions continue to be as much a political and (parochial) economic exercise as a military one.

European firms have not stood idly by while the US competitors have targeted the region though, and they have gained their own CEE foothold. They have found success by targeting countries like Hungary, who recently purchased helicopters from Airbus along with tanks and howitzers from KMW.

While this is smaller than recent US sales, Western European contractors have an advantage: time. Every programmatic delay buys more time for the EDF to mature, extend its tendrils into every Western European foothold in the region, and bring the promise of increased industrial participation.

Thus, absent a dramatic softening of the US tech transfer regime, American contractors will need to push for more creative ways to provide credible differentiation from Western European competitors.

aggressive releases of Excess Defense Articles.

While older, this equipment still represents a

substantial increase in military capability that many

CEE countries otherwise could not afford."

First, they can take advantage of the upcoming eastern shift of US operations in the region and establish logistics and maintenance centers that are able to serve both a country’s new equipment and US forces in region, in a model similar to the F-35’s maintenance depots in Australia, Japan, and the United Kingdom. This expands NATO’s operational support footprint into the region and grants CEE countries access to a much larger sustainment enterprise.

Second, American firms should push for more aggressive releases of Excess Defense Articles. While older, this equipment still represents a substantial increase in military capability that many CEE countries otherwise could not afford.

This has been seen in Croatia, where 16 retired OH-58 Kiowa Warriors are providing the country with new capabilities it could not afford (and now cannot afford to replace) and a pair of UH-60Ms donated to the Croatia Special Forces have introduced the platform to the Croatian military ahead of an eventual Mi-8/17 replacement program. These introductions induct CEE customers to US-style CONOPS and equipping standards that increase switching-costs to European competitors.

Finally, American contractors should extol the wider advantages of buying into the US defense enterprise. The opportunity to tap into the extensive US training enterprise during and after the acquisition process would be a boon to CEE nations overhauling their militaries.

While this has most recently been highlighted by international F-35 customers conducting their initial training at Luke Air Force Base amid the expansive Western US training range infrastructure, it is an opportunity that can be granted to non-Air Force customers, particularly given the establishment of a new Combat Training Center in Drawsko Pomorskie, Poland.

Meanwhile, the Foreign Military Sales process grants international contractors access to DoD buying power, not only for the acquisition itself, but also for the all-critical procurement of spare parts and weapons reloads decades down the line.

As they pursue long-overdue military modernization CEE countries will have to balance competing economic, political, and security imperatives. While going with US defense prime contractors provides top-tier capability and stronger ties with the only NATO member that can credibly deter Russian military adventurism, Western European firms will offer the lure of technology sharing and a more lucrative package for local industry. How CEE nations strike that balance will shape the military-political alignment of Europe’s eastern flank for the next generation.