ESG Strategy & Sustainability Best Practices for Government Contractors

Government contractors face unique challenges, as they are typically held to a higher standard of accountability and face more public and regulatory scrutiny. Industry leaders recognize that building and maintaining a reputation as a sound steward of the public trust is essential to competitiveness and long-term survival.

As such, government contractors are often at the forefront of implementing new programs and policies that reflect changing public and government priorities.

Not surprisingly, many government contractors have taken steps to advance ESG strategy and broader sustainability, with these efforts accelerating since 2020. For example, some companies issued their first sustainability report (e.g., HII, Viasat) or first diversity and inclusion report (e.g., BAE, L3-Harris).

Other companies, such as Northrop Grumman and Boeing, have hired Chief Sustainability Officers. Still more announced new initiatives to further advance sustainability and philanthropic activities, such as AECOM’s “Sustainable Legacies” campaign and Raytheon Technologies’ “Connect Up” initiative.

To assess the state of ESG activities of government contractors, Avascent conducted an outside-in review of the ESG strategy and sustainability activities of the top 100 government contractors.

As is the case across most industries, the companies reviewed were often at different states of maturity along their ESG journeys. However, many companies have shown increasing commitment to a ESG strategy.

Recognizing this variability, Avascent identified eight best practices that leading players are adopting as they pursue their ESG strategy and sustainability objectives:

- Leverage materiality assessments or other prioritization approaches to focus management attention

- Implement ESG strategy practices in both internal infrastructure and external business strategy

- Report against voluntary frameworks, such as CDP, SASB, GRI, TCFD, SDG, and/or SBT

- Issue focused ESG or related reports to supplement mainstream reporting

- Incorporate ESG material risks in SEC filings

- Communicate on ESG strategy topics frequently and consistently

- Designate senior leaders and board committees responsible for ESG strategy topics

- Link executive compensation to sustainability and/or DE&I goals

Approach

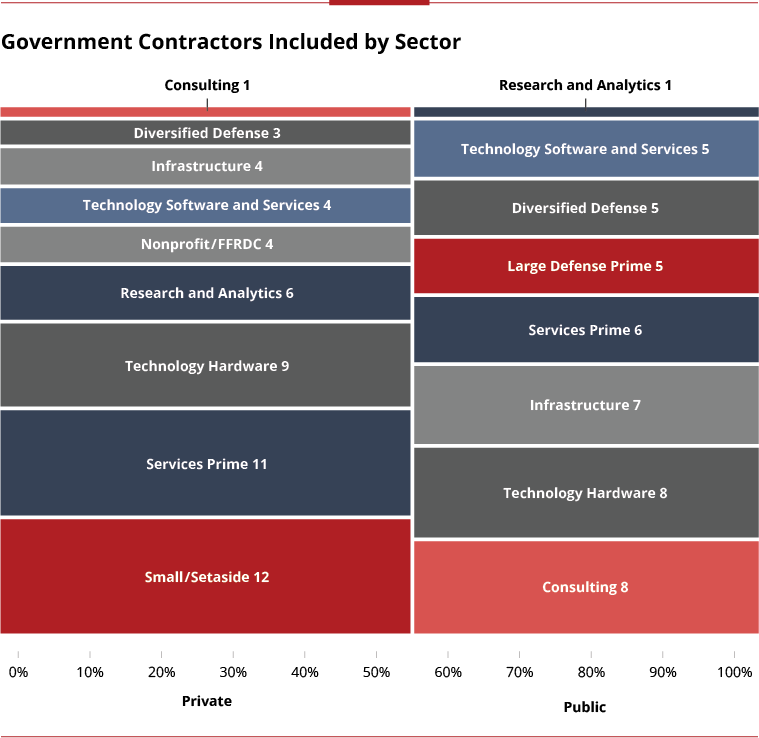

For our sample, Avascent drew on the 2021 Washington Technology Top 100 list of government contractors, which identifies largest government contractors in US federal market by prime obligations. At the time of analysis, there was one company on the list that had been acquired by another company on the list, leaving 45 public companies and 54 private companies.

As the figure below indicates, these firms spanned a wide range of product and service categories, producing everything from defense equipment to software, as well as providing a wide range of technical and support services.

To assess the ESG strategy activities of these companies, Avascent reviewed publicly available information (e.g., company website, SEC filings, earnings calls, news releases). Given that these many firms may have non-public initiatives underway, this portrait of the full spectrum of their activities may be constrained.

However, it provides a useful comparison point across a broad spectrum of firms. In all cases, this analysis drew on each company’s most recent available data.

While Avascent assessed both private and public firms, there was some information that was only accessible for public firms (e.g., earnings call analysis). Therefore, some data points only consider public firms and will be noted as such throughout the analysis.

Industry Best Practices

In reviewing the results of this analysis, Avascent identified best practices across three broad topic areas:

- Sustainability & ESG Strategy

- Data Collection & Reporting

- Organizational Investments and Incentives

Sustainability & ESG Strategy

1. Leverage materiality assessments or other prioritization approaches to focus management attention

Research suggests that companies that focus on material ESG issues, or ESG strategy issues fundamental to the long-term success of the company, see the highest return from their efforts. Companies that act on both material and immaterial ESG issues tend to see lower returns than if they had prioritized their efforts.[1]

Given the scope of ESG-related issues, it may be tempting to throw spaghetti at the wall and address every dimension of the problem, but focus is key.

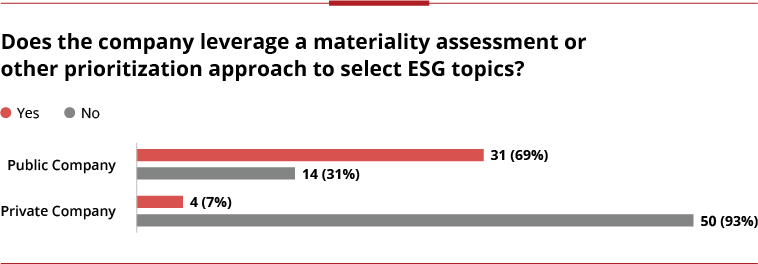

One type of analysis that can help companies identify material ESG issues is a materiality assessment, an exercise that helps identify ESG strategy issues that will have highest impact on the business and are of greatest importance to critical stakeholders.

In our analysis, we found that almost 70 percent of public companies presented evidence that they leveraged a materiality assessment or some other prioritization approach. In contrast, only seven percent of private companies did so.

This suggests that a sizable number of government contractors, and particularly those not exposed to public markets, may be trying to tackle too many ESG topics at once or are investing in addressing immaterial issues.

When reviewing the ESG strategy topics prioritized by companies, there was a clear pattern regarding the most frequently cited topics. Companies covered a broad spectrum of “social” topics, with firms most frequently highlighting activities related to community engagement and philanthropy and diversity, equity, and inclusion (DE&I) initiatives.

Given the overlap with more traditional regulatory reporting requirements, governance-related topics were also heavily emphasized, ranging from ethics and cyber security policies to supply chain management. Finally, environmental-related topics were focused on climate change and decarbonization.

As would be expected, companies tended to focus most on topics closely related to their core business. Services firms tended to place greater emphasis on human capital related issues, while product manufacturers and infrastructure businesses tended to focus more closely on environmental issues.

![]()

What ESG Strategy topics were prioritized by firms?

2. Implement ESG strategy practices in both internal infrastructure and external business strategy

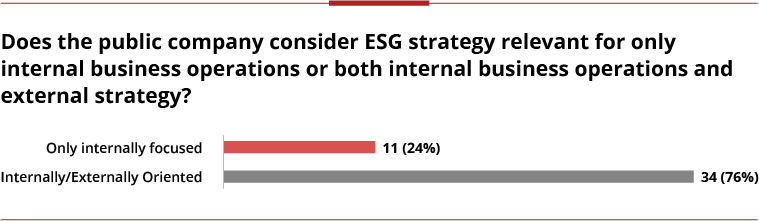

Avascent’s research also suggests that the most innovative leaders recognize that their sustainability & ESG strategies must face both inward and outward. Internally, ESG strategy focuses on key business operations. Externally, firms are evaluating how to integrate ESG and sustainability into their business and product strategy.

Avascent found that 24 percent of public companies reviewed had an ESG strategy that was only focused on its internal business operations. These strategies tended to be more mature as they focused on mostly topics such as energy efficiency and recycling.

76 percent of public companies had an ESG strategy that addressed both internal business operations and their external business strategy. Many of these companies identified ESG or sustainability topics as integral to future product and service innovations. They recognize that progress on ESG and sustainability is crucial to future value creation and not simply limited to risk mitigation. That said, very few of these companies had mature strategies around how such external business opportunities would be developed.

Data Collection & Reporting

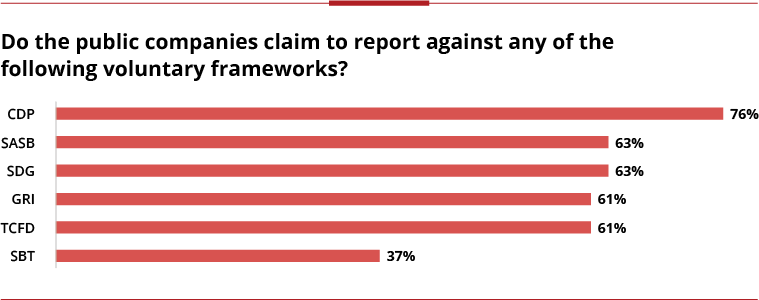

3. Report against voluntary frameworks, such as CDP, SASB, GRI, TCFD, SDG, and/or SBT

With new ESG strategy and/or sustainability disclosures likely to become mandatory over the next few years, many of the leading public companies surveyed have sought to proactively align around some of the leading voluntary reporting frameworks.

These include the Carbon Disclosure Project (CDP), Sustainable Accounting Standards Board (SASB), Sustainable Development Goals (SDG), Global Reporting Initiative (GRI), Task Force on Climate-Related Financial Disclosures (TCFD), and Science-Based Target (SBT) initiative.

Given the proliferation of different standards, it can be difficult to know which standard to embrace, although there are benefits to reporting proactively. For example, there is evidence to suggest that future US mandatory climate disclosures will likely closely resemble existing TCFD frameworks.

Reporting against one or more of these voluntary frameworks can help companies get ahead of future mandatory disclosure and further validate their approach to material ESG issues.

4. Issue focused ESG or related reports to supplement mainstream reporting

Many of the proactive leaders identified during Avascent’s review sought to codify ongoing ESG strategy and sustainability activities through a formal ESG or sustainability report.

Research suggests that capturing and reporting on ESG activities and commitments in public and online can drive accountability.

While these reports provide an opportunity to highlight successes and share best practices, they also provide a benchmark against which internal and external stakeholders measure progress.

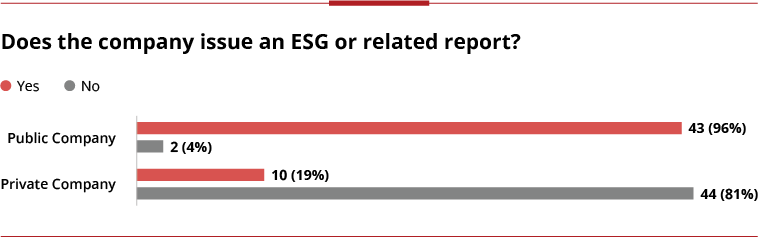

100% of the public companies reviewed and 85 percent of private companies surveyed allocated at least some space on their websites to sharing information on their ESG and related activities (e.g., ethics policy). In addition, most (96 percent) public companies also produced more formal ESG strategy or sustainability reports. In contrast, only 19 percent of private companies issued such reports.

5. Incorporate ESG material risks in SEC filings

Beyond issuing their own reports, many public companies surveyed also incorporated relevant ESG material risks in their regulatory filings (e.g., 10Ks). This is in line with the recommendations of frameworks such as TCFD, which endorses disclosing any ESG topics deemed material as part of a public company’s normal reporting processes.

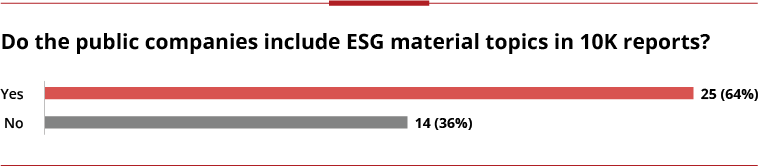

Avascent reviewed 10Ks for 39 of the 45 public companies in our survey (the other companies were based outside of the United States and not subject to the same reporting requirements).

Of these, 36 percent did not mention any ESG or sustainability-related risks in the 10K despite often recognizing these ESG topics as material to the business in their ESG strategy report.

While the other firms did include some mention of ESG topics in a risk section, these companies often limited their discussion to impending disclosure regulation or risk of ongoing environmental legislation.

6. Communicate on ESG strategy topics consistently and frequently

If company leaders see ESG strategy topics as material to future business strategy and value, it is likely that they will discuss these topics during earnings calls and in other public channels. It is important to consistently and frequently communicate on these topics.

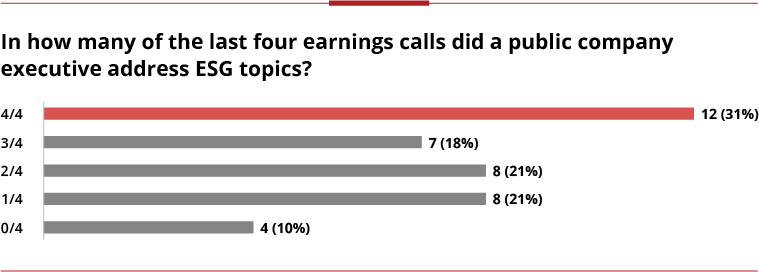

One channel for company executives to communicate on these topics is earnings calls. Of the thirty-nine US-public companies examined, 12 of these companies discussed ESG strategy topics in all four of their last four earnings calls.

In contrast, leaders of four companies surveyed did not discuss ESG topics once during their last four quarters. Executives were more likely to raise these issues during their prepared initial statements than when responding to questions from analysts.

Organizational Investments & Incentives

7. Designate senior leaders and board committees responsible for ESG strategy topics

When developing an effective ESG strategy, firms need to designate someone in leadership to be the ultimate owner of the initiative. Ideally, this should be a senior leader with real clout, is a member of the executive committee, and reports directly to the CEO.

78 percent of the public companies reviewed had identified a senior leader as the firm ESG champion, even if the internal reporting relationships were not always clear.

These senior leaders came from a mix of functional areas, including human resources, operations, and finance functions.

While some of these leaders were “dual-hatted” with other responsibilities, 13 of the 45 public companies surveyed specifically hired a Chief Sustainability Officer with sole responsibility for advancing the firm’s sustainability and climate strategies.

In addition to identifying an ESG champion, firms should ensure that relevant issues are regularly reviewed and addressed by the Board. Ideally, the Board should designate a specific committee to monitor these topics and drive long-term firm value.

Of the public companies reviewed, 78 percent had clearly designated one or more Board committees as responsible for addressing ESG strategy and sustainability topics. Some companies have even launched a new Board committee (e.g., Sustainability Committee) specifically to oversee the firm’s performance in these areas.

8. Link executive compensation to sustainability and/or DE&I goals

To ensure that their executives ultimately feel that they own the outcomes of ESG strategies and goals, many companies reviewed had tied performance against these metrics to executives’ financial incentives.

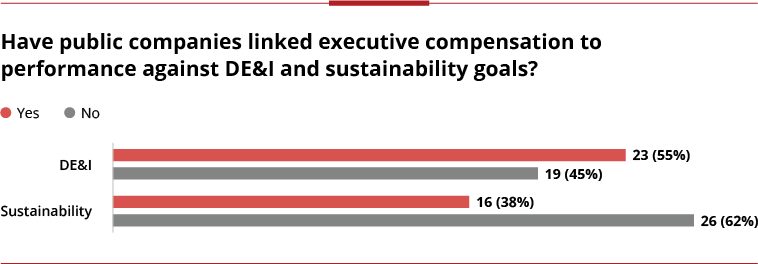

Avascent reviewed 14F shareholder reports to analyze whether sustainability and DE&I were included as compensation criteria for senior executives.

Of the forty-two companies that had filed this information, 55 percent included DE&I as an explicit performance metric. In contrast, only 38 percent included sustainability as part of the criteria for assessing executive performance.

Conclusion on ESG Strategies and Sustainability Best Practices

A growing number of government contractors have made real progress and investments to position themselves as ESG leaders.

However, even these ESG leaders are continuously evolving their ESG and sustainability strategies. The process of building and implementing a robust internal and external sustainability and ESG strategy may take years, but can start with simple, incremental steps today. This journey is important not only to mitigate risk, but also to capitalize on emerging market opportunity.