SHARPE Focus: The Recent Emergence of Defense Unicorns

Tech Investor’s New Focus on National Security

The world is changing rapidly, and all branches of the US military are making fundamental changes in how they address a dynamic threat environment.

The 2023 Department of Defense Presidential Budget Request indicates a sustained focus on modernization, particularly on breakthrough technologies sourced from a more diverse and agile industrial base.

Within the last twelve months, four defense technology start-ups raised capital at $1 billion-plus valuations.

This group of companies is part of a broader cohort of defense unicorns that we refer to as the “SHARPE” cohort:

- Shield AI,

- HawkEye 360,

- Anduril,

- Rebellion Defense,

- Palantir (now public), and

- Epirus.

These companies are focused on applying cutting-edge technologies—AI, machine learning, big data, autonomy, and others—to national security challenges so the US can retain overmatch capability against its adversaries.

From a private capital allocation perspective, the recent emergence of SHARPE companies is noteworthy. After a multi-decade hiatus, Silicon Valley investors are once again seriously focused on the market opportunity within national security, and blue-chip venture firms are investing significantly in defense technology, signaling potential in the future of the defense market.

Will SHARPE investor interest last?

While interest is strong at the moment, will it remain so over the long term?

In exploring this question, we found several parallels between the automotive and defense markets and, specifically, the relatively recent but now material impact that “new auto” tech companies are having upon the auto sector.

- Both industries are mature, consolidated, and historically dominated by industrial champions: Toyota, GM, and Ford within automotive and Lockheed Martin, Northrop Grumman, and Raytheon within defense.

- These longstanding OEMs have enjoyed strong positions within finite addressable markets generally characterized by low yet predictable growth. Within auto, that market has been cars per household, with growth tied to GDP and household income. Within defense, the market is defined by the Department of Defense (“DoD”) budget, with growth pockets ebbing and flowing across platforms as strategic priorities change. Because of their focus on well-defined, incumbent platforms, auto and defense OEMs have unintentionally hindered their ability to rapidly innovate.

- Finally, both industries have seen the rise of software-defined systems, which has opened the door to new players offering innovative solutions.

Three Metrics to Assess SHARPE’s Impact

How can an investor quantify the impact the SHARPE cohort is having on the defense industry? Three metrics demonstrate the transformative impact new auto has had on its market:

- Largest companies by market capitalization,

- Share of market capitalization, and

- Time to valuation.

By evaluating the SHARPE cohort against these indicators, investors can assess the scale and pace of their disruptive role in the market.

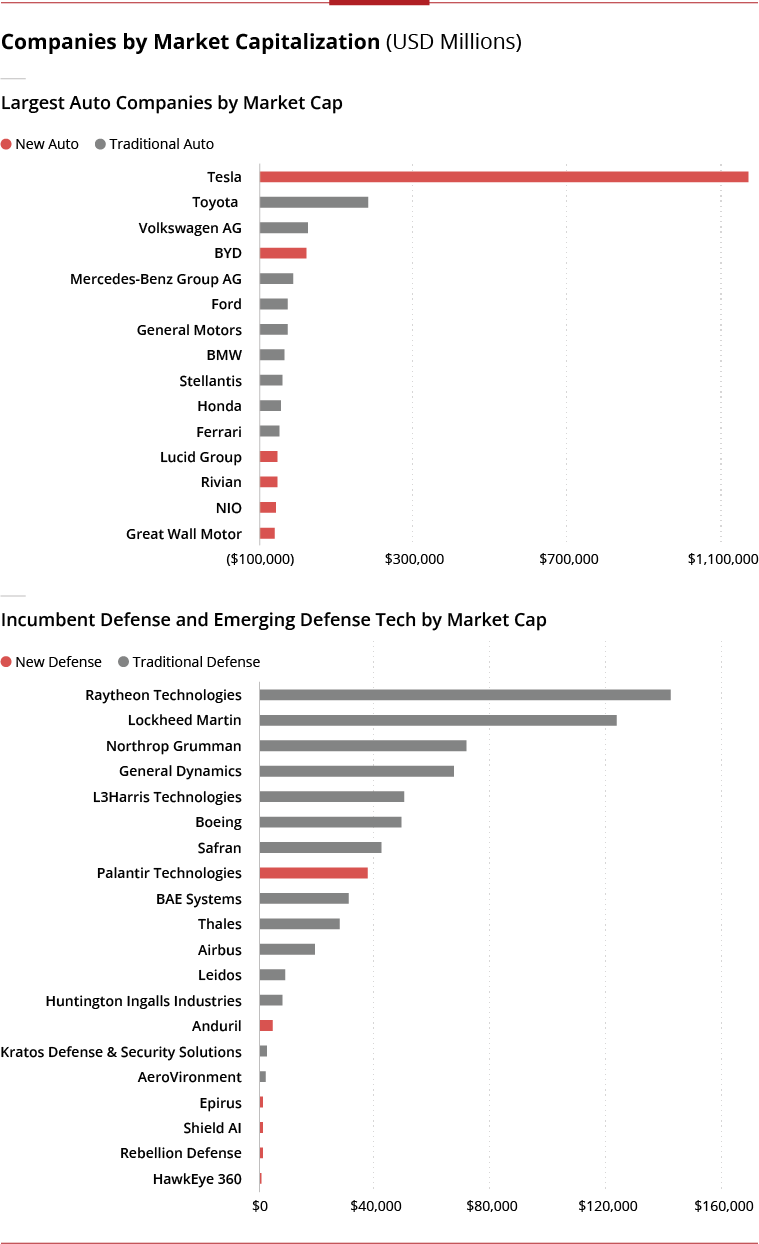

1. Largest Companies by Market Capitalization

Within the last several years, valuations of public companies focused on next-generation automotive technology have risen steeply.

Today, the market capitalizations of five auto tech companies (Tesla, BYD Company, Rivian, Lucid, and NIO) place them among the fifteen largest auto companies in the world.

Just as the enduring emphasis on automotive technology and rise of electric vehicles has propelled the growth of new auto, DoD modernization priorities are focused more than ever on capabilities such as geospatial analytics.

Such capabilities tend to benefit from commercial applications and development, and typically are developed by newer, more agile players. [1] [4]

Moreover, the proliferation of organizations (e.g., AFWERX, DIU) and funding mechanisms (Small Business Innovative Research Grants, Other Transaction Authority) focused on accessing new tech is easing entry for new defense players into the DoD ecosystem.

2. Share of Market Capitalization

Manufacturers focused on electrification, most notably Tesla, have captured significant market investment from traditional OEMs. Today, they own approximately 50% of the automotive industry’s aggregate market capitalization, while accounting for only 9% of new vehicle sales. [2]

Unlike new auto, SHARPE companies account for only ~7% of the aggregate defense market capitalization and similarly have not achieved market capitalization parity like BYD and Rivian or domination like Tesla.

However, Palantir’s growth and position as a prime on large-scale programs of record like Distributed Common Ground System-Army provides a potential model for SHARPE’s successful competition with the legacy giants.

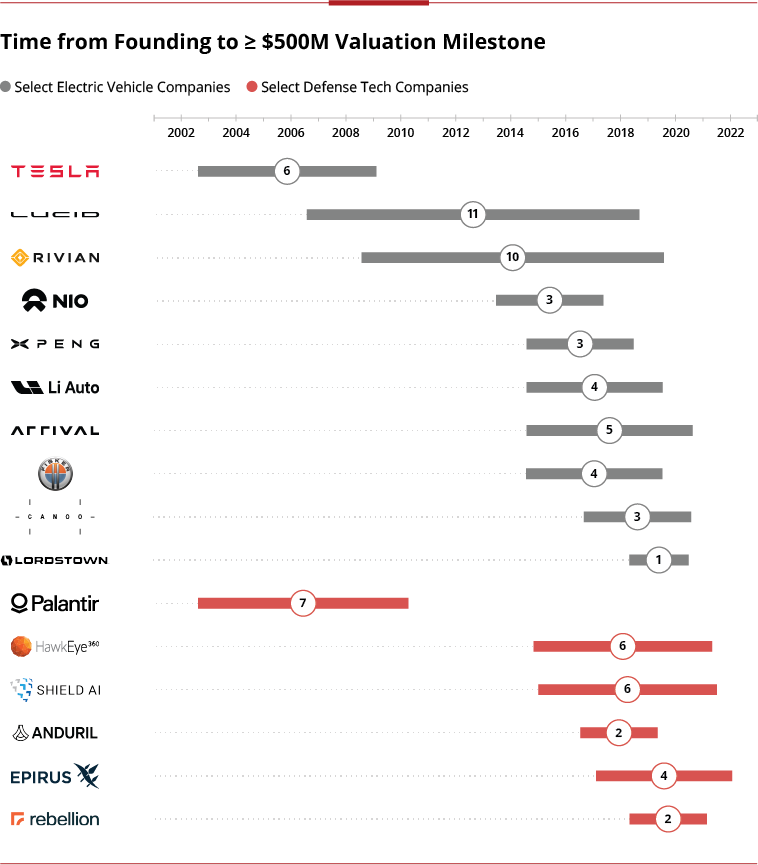

3. Time from Founding to ≥ $500M Valuation Milestone

Spiking new auto valuations and growth reflect not only shifting industry priorities and consumer preferences but also the expansion of an auto-oriented manufacturer’s addressable market beyond traditional applications.

At the forefront of the auto tech revolution, Tesla and Lucid Group surpassed $500M+ valuations in six and eleven years, respectively.

Since then, auto tech companies have been surpassing the $500M valuation milestone in increasingly shorter timespans as investors recognize the value being created by the paradigm shift underway in the industry.

Much like Tesla and Lucid Group in auto tech, Palantir was an early mover within defense tech, achieving a $500 million-plus valuation in seven years.

Following Palantir, SHARPE companies have been achieving $500 million-plus valuations in relatively expedited timeframes despite their early-state or relatively unproven technologies, similar to trends within automotive technology.

Recently, Anduril and Rebellion Defense surpassed this threshold within two years of their respective formations. [3]

Current valuations of these defense tech players reflect investor focus on a longer-term strategic vision, with multiples often tied to earnings that are projected for several years in the future, and an expectation that these innovators will capture significant share from legacy defense OEMs.

Valuing SHARPE: Assumptions & Questions

With SHARPE here to stay, these early unicorns will continue to attract investor attention and additional players will seek to raise capital at similarly strong valuations. How should investors think about the staying power of early entrant valuations and the valuation of new entrants?

In theory, private market valuations for SHARPE companies should depend on the two variables used to value incumbent defense behemoths: future cash flows and total addressable market (“TAM”).

Additionally, investors should consider the extent to which the SHARPE cohort can materially gain share in key segments against traditional primes, and how commercial markets could broaden their TAMs.

1. Cash Flows:

Future cash flow for SHARPE is an open question. The US Government (“USG”) has historically approached procurement under rules and regulations different than those in the commercial sector.

- Even if a defense start-up has dominant game-changing technology or proprietary software, will the USG allow it to realize the extraordinary market positions and levels of profitability achieved by the likes of Google, Facebook, or Apple?

- Or will the USG ultimately cap acceptable profit margins, enforce data rights sharing, etc., all of which could fundamentally alter the future cash flow prospects of these defense start-ups?

2. Total Addressable Market & Market Growth:

Even with a 4% topline increase in FY2023 Presidential Budget including a 10% increase in research, development, test, and evaluation (RDT&E) funding over 2022, defense budgets are relatively well-defined and capped compared to other markets.

- How will SHARPE convey TAM upside to investors?

- Will new technologies simply displace existing capabilities and platforms?

- Or will they fundamentally transform how budgets are deployed – for example, sacrificing force structure and divesting aging platforms to invest in software, unmanned systems, high volumes of low-cost sensors, or similar platforms?

Most likely, the large, needle-moving DoD programs will remain platforms and systems owned by primes. However, the stated criticality of new defense technologies like artificial intelligence and cybersecurity to nearly every DoD mission and system indicates these technologies will be embedded in large enterprise and mission systems.

New defense companies can thus portray TAM as a percentage slice of whole segments, reducing pressure on winning near-term, large-scale programs. This approach also reduces investor expectations of and visibility into “make or break” opportunities.

3. First Mover & Market Segment Leadership:

With nearly limitless applications for new defense technologies across DoD programs, investors must look to differentiators between the hundreds of new players securing footholds in DoD dual-use technology investment.

First-mover advantage in key emerging segments, as demonstrated by Hawkeye 360 in RF geoanalytics and Shield AI in unmanned systems artificial intelligence, may become a key driver of perceived value.

- Will valuation become more reliant on leadership within a high growth segment like counter-UAS rather than market share versus OEMs?

- Does valuation reflect a scarcity value in these segments, and will the subsequent emergence of new start-ups in each segment dilute that scarcity premium?

4. Hardware Hook to Scale:

In response to new auto moves, traditional auto manufacturers are working to strengthen software-defined vehicle capabilities through a mix of partnering (e.g., Toyota and AWS, Hyundai and Aptiv), bolstering internal expertise (e.g., Volkswagen), and reorganizing P&Ls (e.g., Ford split into a gasoline-powered and EV-powered segments).

SHARPE should expect to see both countermoves and partnering outreach from traditional primes seeking to contain, exploit, or propel the disruptive impact of innovation.

Just as traditional primes are looking to harness commercial technology, SHARPE may need to bolster access to “traditional” technology to compete more like an OEM in the DoD market.

Several of the SHARPE companies have made moves to acquire a “hardware hook,” as in Shield’s acquisition of Martin UAV and Anduril’s acquisition of Dive.

- Will a hardware hook be table stakes for SHARPE looking to scale and compete head-to-head with defense OEMs?

- Will SHARPE depend on the partnership and pull-through of the traditional integrators to gain access to the platforms and systems ripe for digital transformation?

- Or will they find new ways of demonstrating growth potential to investors?

5. Commercial Upside:

It is also possible that defense start-ups could introduce technology with future applications within the broader commercial market that dwarf the size of their initial use cases for national security applications.

Potential examples include commercial electric vertical take-off and landing vehicles (“eVTOL”) extensions of defense autonomy pursuits, and commercial infrastructure protection extensions of counter-UAS software.

By extension, SHARPE valuations may not be strictly defense multiples, instead representing the potential to expand into larger commercial end markets.

Will the Market Continue to Believe in Defense Innovation?

As the DoD shifts focus to near-peer adversaries, technological innovation is essential to maintaining the US’s global position. The DoD has increasingly turned to start-ups and Silicon Valley to catalyze innovation.

Recent history within the automotive market provides a potential template for similar growth and rapid innovation within the defense space.

However, an important distinction within the two markets is the role of government. The current USG acquisition and contracting process significantly impacts adoption rates, feedback cycles, and profitability and growth potential of defense suppliers.

Meaningful improvements to that process would be enormously beneficial for both the market and national security, and while the likelihood for timely improvement of the procurement process is uncertain, the substantial capital investment to date and current valuations of SHARPE signal overall investor optimism in the future potential of defense technology.

About Avascent and Harris Williams

Avascent is the leading strategy and management consulting firm serving clients operating in government-driven markets. Working with corporate leaders and financial investors, Avascent delivers sophisticated, fact-based solutions in the areas of strategic growth, value capture, and mergers and acquisition support.

Harris Williams’ Aerospace, Defense & Government Services (ADG) Group combines deep industry knowledge and relationships with superior M&A advisory services. As a pure-play advisor with no conflicts of interest, our ADG Group offers differentiated strategic advice and seamless execution to a global base of leading aerospace, defense, and government services clients.

Footnotes:

[1] S&P Capital IQ

[2] IEA, Global sales and sales market share of electric cars, 2010-2021, IEA, Paris https://www.iea.org/data-and-statistics/charts/global-sales-and-sales-ma…

[3] Pitchbook

[4] Defense company market capitalizations reflect the portions attributable to defense revenues