Defense Spending and COVID-19: Implications and Impact on East Asian Government Finance and National Security

The future impact of the COVID-19 crisis on defense spending in Asia is challenging to gauge.

The basic strategic calculus in the region remains unchanged – with China and North Korea driving many regional powers to invest in advanced capabilities. But the depth the economic downturn will have fundamental effects on government spending.

The costs of combatting COVID-19, both the near-term health crisis and the mid-term economic dislocation, will create pressure on defense spending that few governments will be able to avoid. Defense budgets will likely become bill payers.

But East Asia has weathered financial crises before, with very different degrees of impact on defense spending.

Only time will tell whether this crisis will affect defense spending along the lines of the 1997 financial crisis, or closer to the 2008 financial crisis.

The former had a big and sustained impact on defense spending, where the latter imposed a much more modest pause in growth.

Figure 1: East Asian (ex. China) Defense Spending, 1995-2014

USD Millions

This paper is the second in a series that Avascent is generating to explore how the COVID-19 pandemic may transform the global defense market and competitive landscape.

To be sure, the global health and economic situation is still unfolding, and the true extent of the economic and social fallout is remains uncertain. But we offer our thoughts at this moment to help planners in government and industry begin to prepare for various outcomes.

Range of COVID-19 Response Across Asia

Many Asian countries feature large urban centers with high degrees of population density, which can increase the risk of COVID-19 transmission. Some of the earliest orders to lock down cities were seen in Asia.

Fortunately for some Asian countries, government response to the pandemic has been more effective than those seen in Europe and the United States.

As a result, the infection rates in some countries like South Korea and Taiwan are significantly lower than those seen in the West.

For these countries, early and aggressive containment measures in response to the pandemic could mean relatively less severe economic damage and a stronger recovery coming out of the pandemic.

But containment measures have been varied in timing and scale across Asia.

Indonesia and Japan were slow to roll out testing and population lockdowns due to lack of central coordination and reluctance to suppress economic activity.

Singapore is notable in that it initially appeared to have successfully contained the spread of the virus through strict contact tracing and travel restrictions. But repatriated Singaporeans brought back the virus from abroad, sparking a second infection wave and stricter social distancing measures.

The biggest risk of spikes in COVID-19 cases are among Asian countries that have dense cities with large, impoverished populations with poor access to healthcare and limited options for effective social distancing.

Cities like Jakarta and Manila have urban areas with sprawling slums and populations much larger than those of most European cities. If these dense cities experience infection rates similar to those seen in Europe, it would constitute an unmitigated public health disaster.

Tracking the spread of infection in these areas has been very difficult, meaning actual cases may be much higher than reported.

Economic Conditions and Implications for Government Spending

In East Asia, where the pandemic started, the impact on government spending will be influenced in part by each country’s underlying economic situation.

The region features a varied mix of economies, with both highly advanced nations like Japan, South Korea and Taiwan, as well as emerging economies in Indonesia, Malaysia, the Philippines, and others.

These emerging countries have fewer resources to draw upon, which may increase pressure to shift resources from defense to public health, income support, and economic development.

Governments in these developing economies had already prioritized economic development in their budgets before the pandemic. Drawing down defense budgets to pay for economic stimulus and emergency response will be politically important.

Indeed, Indonesia has already reallocated $535 million from its 2020 defense budget to other ministries help with pandemic response.

A broader issue that will impact not just East Asia but many countries worldwide is debt. South Korea’s announced reallocation of $730 million from its defense budget hints at the debt issue.

The shifted funds were to contribute to an emergency $6.27 billion supplementary budget that the government aims to fund without the issue of new debt. As governments across Asia and the world draw up huge economic stimulus packages, government debt is set to rise.

This will raise concerns about how much governments will need to spend on servicing debt that has ballooned in the wake of COVID-19, in turn raising questions about how governments will continue to fund other priorities in economic development, healthcare, as well as defense.

If governments try to control spending by balancing their budgets, that could further limit spending on defense.

the more fiscal pressure governments in both

developed and developing East Asia will feel,

potentially constraining defense spending growth."

While rising debt will be a worldwide concern going forward, a more current issue is focused on the global slump in trade. Many Asian economies are highly dependent on foreign trade as a source of income and a key contributor to economic growth. For example, exports make up 173% of Singapore’s economy, pointing to how exposed

it is to trade shocks. The Singaporean defense budget growth has slowed since the US-China trade war began, dropping from an average growth rate of 5% between 2014 and 2017, to just 2% from 2018 to 2020.

Even for developed economies that have lower exports to GDP ratios, such as Japan, South Korea, and Taiwan, trade is a key part of their economic growth strategies, especially as their populations age.

The longer the global economy takes to recover, the more fiscal pressure governments in both developed and developing East Asia will feel, potentially constraining defense spending growth.

COVID-19’s Impact on the Security Environment in Asia

The pandemic’s effects will likely result in changes to defense spending and acquisitions, as emergency response and economic stimulus become greater government priorities among many countries in the region. But the overall strategic disposition of the region is unlikely to change significantly.

In East Asia, China will continue to expand its military forces and push its territorial claims. To be sure, the Chinese economy in 2020 looks set to contract for the first time in decades, following a long period of rapid growth. Nevertheless, we assume that China’s financial wherewithal will remain very high, along with its ability to overawe its neighbors.

We assume that North Korea’s leader will remain firmly in control, and undeterred from developing nuclear and long-range missile capabilities.

Despite appearing to recover from his latest bout of poor health, it is surely feasible to consider scenarios in which Kim Jong Un succumbs to illness in the future (and whatever other ailments the overweight and chain-smoking dictator may have).

But it is hard to imagine Kim being replaced by leaders who would pursue a quick transition to a fundamentally different relationship with North Korea’s neighbors or the United States.

Consequently, Japan, South Korea and Taiwan, will have the most reason to avoid cutting defense spending too deeply, considering their proximity to North Korea and China. Even if some reductions in defense spending are made, the persistence of these threats raise the floor of how much defense spending can be reduced.

As for Southeast Asia, piracy, smuggling, and illegal fishing could see a temporary downturn due to the decrease in shipping traffic and global consumption. There is no reason to believe these will not return to prior levels once global economic activity recovers. The question will be how long it takes for global demand to return to earlier levels, the answer to which no one is certain yet.

Finally, the United States seems intent on retaining its role in East Asia security. The Trump Administration and many other US politicians view China as culpable for failing to contain the spread of Coronavirus or apprise the world of the risk in

a timely way.

This is building on a broader sense of concern for China as a potential threat, which was already piqued by the trade war, concern for Huawei’s influence over global 5G technology, and other developments.

The US Congress is actively weighing in increase in fiscal year 2021 spending specifically to bolster DoD capabilities to confront China in East Asia. This should influence the thinking on the part of Japan, South Korea, and Taiwan, in terms of taking near-term risk in their own defense expenditures.

Potential Upside Effects on Defense Spending from COVID-19

Despite the negative impacts COVID-19 may have on defense spending in the region, there are some factors that could offset pressure to cut defense budgets. The loss in jobs due to decreased global demand has governments struggling to find ways to keep businesses operating and citizens employed.

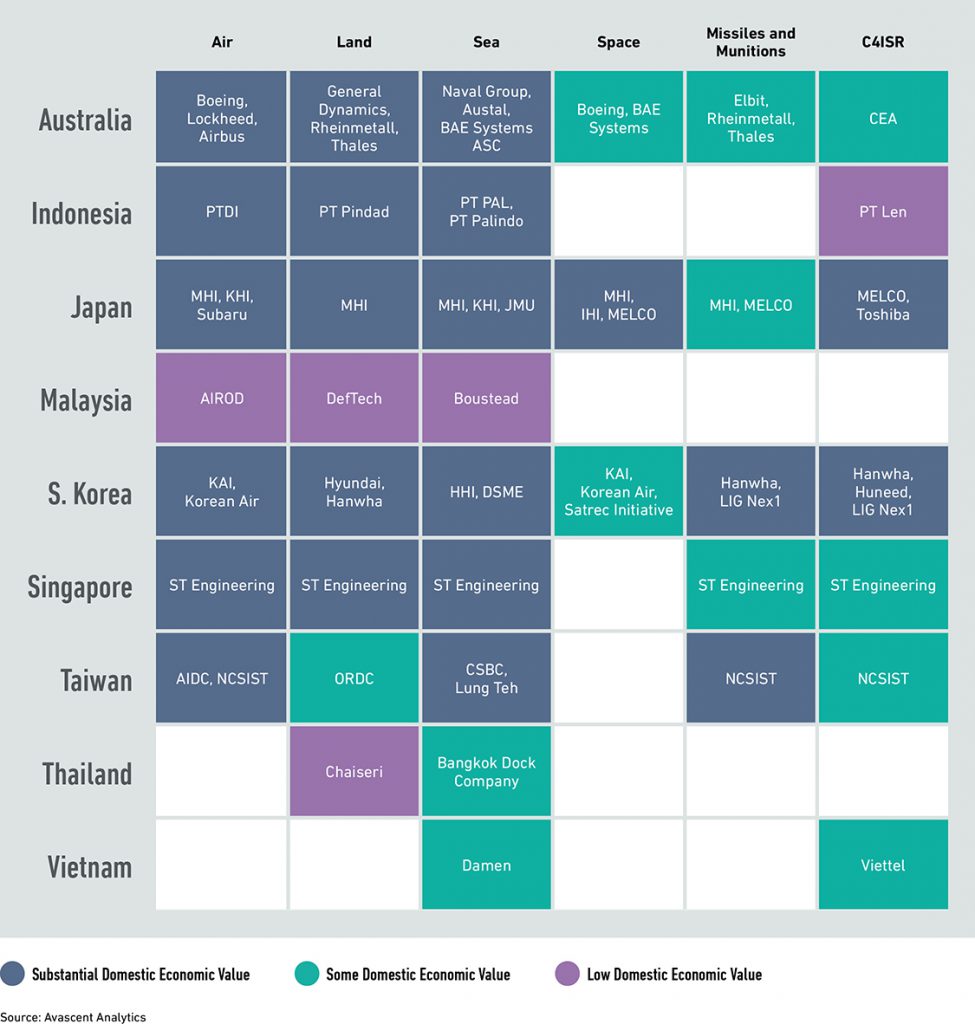

Those countries with a significant defense industrial base – Japan, Singapore, South Korea, and others – may look to expanded defense spending to sustain employment.

One way to do this would be to continue signing contracts for defense procurements involving local engineering, production or sustainment. In a sense, defense contracts can serve as a form of government economic stimulus, as these contracts will help keep factories operating and people employed.

For some large companies like Mitsubishi Heavy Industries and Korea Shipbuilding & Offshore Engineering (formerly Hyundai Heavy Industries), which derive as much as 85 percent of their sales in the commercial sector, defense sales may mitigate some losses.

Many countries in Asia were already strongly pushing to bolster their local defense industrial bases and increase the number of companies and workers involved in defense production.

Figure 2: Defense Companies as Major Employers Among Selected Asia/Pacific Countries

In East Asia, both geography and climate serve to make military forces a significant player in disaster response. The Asia-Pacific region’s geography makes the region very disaster-prone.

Typhoons, earthquakes, tsunamis, volcanoes, in addition to epidemics, have all made significant scars on Asia in the past decade. Geography also makes the logistics of disaster response highly difficult.

Many countries are made up of island chains or are divided by mountains and dense forest. Infrastructure to these isolated regions is either limited or nonexistent.

Past catastrophes like the 2011 tsunami in Japan, Typhoon Haiyan in the Philippines, and the recent Australian bushfires, all saw military airlift, sealift, and logistics play major roles.

The COVID-19 pandemic is only the latest disaster that has demonstrated the value that the military brings in disaster response and relief. Governments around the world will be re-thinking how well prepared they are for the next disaster and whether they are equipped to respond effectively.

that has demonstrated the value that the military

brings in disaster response and relief."

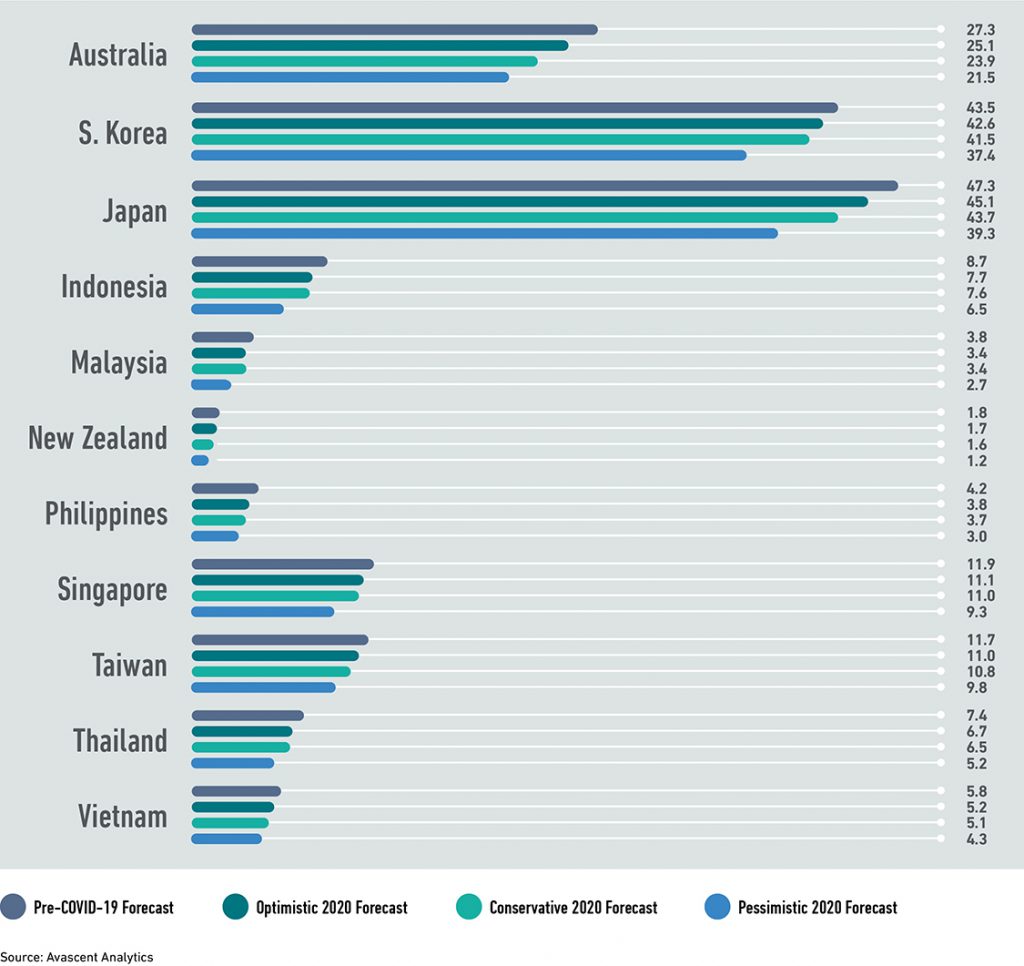

Scenarios for Changes in Defense Budget Growth

We cannot yet know how severe the COVID-19 pandemic will be in each country, or the depth and duration of the economic downturn.

Thus, it seems appropriate to pose a series of scenarios for how defense spending among East Asian countries may shift from our current expectations. We have chosen the year 2020 as the basis for these scenarios, even though it is still underway.

The reason for this is that several countries, including South Korea, Indonesia and Thailand, have already indicated plans to reduce prior defense spending plans for this year.

Further, Japan, which often bolsters its defense budget with supplemental funding mid-year, still has time to rethink that practice.

On the following page is an initial Avascent estimate of three scenarios for how a series of East Asian and Pacific nations may see their defense spending shift in 2020.

In addition to a reallocation of resources to more immediate COVID-19 priorities, some countries may see a fluctuation in exchange rates that have the effect of curtailing their purchasing power as measured in US dollars.

Figure 3: Scenarios for Pre/Post COVID-19 Defense Spending in 2020

USD Billions

To be clear, the range of outcomes shown here is not intended to be “uniform” across each of the eleven countries shown. Rather some countries may see better or worse outcomes for their defense spending than others, depending on an array of factors that may vary from one to the other.

Effects on Defense Investment (Procurement and R&D) From COVID-19

Near-term decreases in defense spending among Asia/Pacific countries are likely to affect procurement and R&D programs. Imported equipment could be the first targeted for cuts or delays as governments try to favor domestically produced systems to support local workforces.

South Korea’s defense budget reduction has led to payment or program delays for the F-35A, Aegis Combat System, and Maritime Operation Helicopter-II anti-submarine helicopter procurement. The government has concentrated cuts in these foreign import programs to try to avoid cuts to domestic programs.

Furthermore, the depreciation of many currencies relative to the US dollar, British pound or the Euro will mean that importing equipment from abroad will become relatively more expensive. For the more developed Northeast Asian economies, this could translate into delays in fighter aircraft and missile defense purchases.

In developing nations across Southeast Asia, expensive submarine and fighter procurements will be at greater risk for delays. In all countries, programs that have already performed poorly on cost and/or schedule will also be more exposed to delays or cuts.

Some defense programs are of very high strategic importance for a mix of threat conditions and long-term defense industrial capacity development. In these cases, defense ministries may try to find savings elsewhere before disrupting these “protected” programs.

Some of these could include Taiwan’s submarine development program, Japan’s Next Generation Fighter development program, and South Korea’s KF-X fighter development program.

Shipbuilding programs in Japan and South Korea are likely to be protected also, given the number of people employed in these industries and the key skills and technologies that need to be retained despite the COVID-19 induced recession.

In developing Southeast Asian countries with more limited budgets, defense ministries may not have the luxury of protecting specific programs from reductions.

However, there are some areas where cuts may be greater or easier to make. These include procurements of land vehicles, ammunition and other materiel in support of reduced training exercises, and imported ships and fighters.

Japan’s investment in ballistic missile defense (BMD) capabilities encapsulates the competing impulses that governments will have as they consider the role of defense spending in the midst of a pandemic.

On one hand, BMD fills an increasingly critical security requirement as North Korea tests an increasingly capable panoply of ballistic missiles and nuclear warheads.

Further, Mitsubishi Heavy Industries has played a key role in developing the SM-3 Block IIA BMD interceptor, in cooperation with Raytheon Technologies.

On the other hand, Japan has relied in part on supplementary budgets to support much of its BMD investment activities. These supplementary budgets are typically used to respond to emergency situations like a pandemic.

And despite the role of domestic companies in developing elements of Japan’s BMD architecture, much of this capability will come from imported US materiel.

Supporting Defense Sales in Pandemic Affected Markets

In an environment in which defense ministries face pressure to cut or delay some defense investments, the global market could see shifts in exporter behavior to take advantage of current conditions.

Many governments support their defense firms with export finance support, which should become more common in a period of extremely low interest rates.

Offering second-hand equipment with refurbishment packages may also gain in appeal, allowing western exporters to compete with cheaper Russian and Chinese designs.

Upgrades to existing platforms will be more likely compared to purchasing new replacements. But more important will be the acceleration of a trend that has become central in the global defense market, particularly in Asia.

Specifically, defense exporters will need to enrich their offers of technology transfer and work sharing, across engineering, production and sustainment. Even before the pandemic, many Asia/Pacific governments made clear their intent to build up domestic defense industrial capacity.

Undertaking these kinds of complex transactions can be extremely challenging for traditional exporters for a mix of reasons:

- Their home governments may be reluctant to export advanced defense technologies;

- Finding viable supply chains in-country can be challenging, even in more advanced economies; and

- Exporters worry about enabling the rise of long-term competitors for advanced defense solutions.

But the COVID-19 crisis seems likely to heighten the pressure to engage in this way, and thereby quicken the competitive pace of the global defense market.

Looking Ahead

In subsequent white papers, Avascent will outline its revised forecast for defense spending and investment among countries in Asia and the rest of the world.

The team at Avascent Analytics, which forecasts defense markets for clients in industry and government, is weighing the economic, political, public health, and security developments that the COVID-19 pandemic has set in motion.

The uncertainty around these issues – and the kinds of competing influences they can have, as evidenced in this discussion of East Asia – may lead our team to begin with a range of budget scenarios.

We will use these to help our clients anticipate how the security and market environment is changing under an unprecedented set of events.