Power Play: What the United Technologies Rockwell Collins Merger Means for the Commercial Aerospace Industry

In one of the largest aerospace acquisitions on record, UTC agreed to acquire Rockwell Collins for $30B on September 4th, 2017. Assuming the United Technologies Rockwell Collins merger is executed, it will create a component supplier with nearly unparalleled scale and portfolio breadth, and it will further aggravate growing tensions between aircraft manufacturers and their primary component providers.

It also has the potential to stoke further industry consolidation and repositioning among mid- and lower-tier players. Corporate leaders will be increasingly challenged to maintain existing sales and margins, preserve customer and supplier relationships, and evaluate new pathways to growth in this quickly evolving environment.

Why Now?

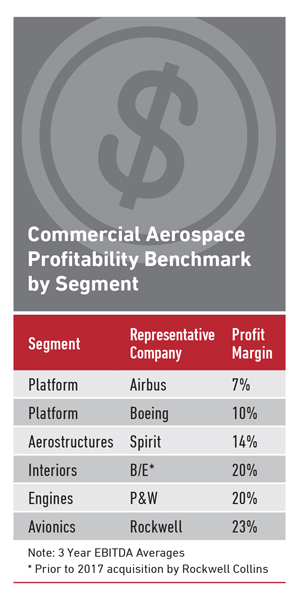

The United Technologies Rockwell Collins merger can be best understood as a reaction to growing tensions between aircraft original equipment manufacturers (OEMs) and their supply base. This tension predominantly stems from significant profit margin differentials; by assuming the bulk of program risk and development costs, aircraft OEMs have been left with typically just half of the 15-20% margins commonly enjoyed by their component providers.

Consequentially, aircraft OEMs have taken an aggressive two-pronged approach to rebalance industry profitability: force significant prices concessions on the supply base, and capture a more dominant share of the lucrative aftermarket.

OEM Pricing Pressure

OEM Pricing Pressure

Over the past half-decade, Boeing and Airbus have made the most visible and concerted efforts to improve profitability by forcing cost reductions on their supply chain.

In 2015, Airbus started an A320-focused program known as SCOPe+ to reduce supplier prices by at least 10%.

This came on the heels of the 2012 launch of Boeing’s similar Partnering for Success (PFS) initiative. PFS offered a simple, yet grueling choice to suppliers: shave costs by 15-25%, or risk losing their business with Boeing.

One year into the program, UTC’s Aerospace Systems (UTAS) segment stood its ground and refused to lower its price on landing gear assemblies for Boeing’s new 777X aircraft (due to enter service at the beginning of the next decade).

UTAS’s gamble backfired, however, as Boeing instead selected a lower bid from Héroux-Devtek. This major displacement materialized despite the Canadian company’s legacy focus on smaller landing gear parts and limited experience further downstream assembling landing systems for large aircraft like the 777X.

With its Rockwell Collins acquisition, UTC will seek to leverage its enhanced clout to ward off similar debacles. The new $60B behemoth will boast a product portfolio that spans nearly every major aircraft system, including engines, electrical power, structures, actuation, landing gear systems – and now avionics and interior systems.

This breadth of coverage should improve UTC’s bargaining power, and ideally help reduce the likelihood of price gouging or blacklisting on upcoming programs, such as the “New Midsize Aircraft” (NMA) that Boeing is expected to launch by 2019.

A further hedge against OEM pressures comes from the inherent cost synergies afforded by this merger, which will help UTC maintain profit margins that shareholders have become accustomed to. In this context, it is understandable that executives at UTC and Rockwell Collins have pointed to estimated efficiencies that can generate approximately $500M in savings by 2021.

Assuming UTC can achieve or even exceed this goal – as it did when it purchased Goodrich for $18.4B in 2012 – it will be able to utilize these freed-up resources in a variety of ways. In addition to aforementioned margin preservation, there will also be room for additional internal research and development (IRAD) investments, which will help UTC keep pace with key aerospace technological advancements, such as digital architectures, composite structures, and more efficient engines.

Aftermarket Access

Requiring price concessions from the supply base is not the only tactic that aircraft OEMs are employing to bolster their bottom line. Direct sales of replacement parts to airlines and their maintenance, repair, and overhaul (MRO) entities in the aftermarket are highly profitable for those suppliers with access to design intellectual property (IP).

While aircraft OEMs have historically deprioritized the aftermarket, they are now seeking to vastly increase their role in this margin-rich domain, much to their suppliers’ dismay. Boeing’s recent formation of a dedicated aftermarket business unit, known as Boeing Global Services (BGS), is a clear example of this new strategic direction that poses a significant threat to UTC and other Tier 1 players.

BGS seeks to achieve $50B in commercial, military, and space services revenue by 2026, a lofty target considering Boeing generated approximately $14B in services activity in 2016. One way it can meet this aggressive goal is through greater insourcing of the design and production of commercial aircraft systems that generate substantial demand in the aftermarket.

Wings, nacelles, and flight control actuation are some of the most notable areas where both Boeing and Airbus have recently brought work in-house, not only to lower production costs, but also to retain design IP and gain greater leverage in the aftermarket.

Boeing’s latest manifestation of this strategy came in July 2017, when it set up Boeing Avionics, an in-house avionics unit. This new entity will not only threaten legacy avionics supplier roles – including Rockwell Collins – but also enable greater ownership of aircraft-wide systems data. This will create opportunities for Boeing to enhance its health-monitoring and MRO capabilities and capture larger aftermarket revenue streams over the life of the aircraft.

Increased strategic insourcing, in addition to revamped life-of-aircraft maintenance programs (e.g., Boeing GoldCare), will help Boeing and other aircraft OEMs as they seek to capture additional aftermarket revenue.

While an ever-expanding global aircraft fleet will provide all competitors with greater market opportunity, it appears inevitable that BGS’ attempts to achieve $50B in services revenue will likely come at the expense of UTC and Rockwell Collins’ own aftermarket sales.

In this context, Tier 1 players must look to add scale and capability in the aftermarket to enhance their value proposition and counter future threats.

For UTC, Rockwell Collins opens up new opportunities in avionics and aircraft interiors – segments where UTC lacked a strong presence, yet together represent roughly 20% of annual commercial aerospace aftermarket materials demand, according to Avascent analysis.

While competing in these segments will be more challenging than ever – especially as Boeing Avionics matures – United Technologies Rockwell Collins merger makes them likely better off fighting together instead of going at it alone.

What’s Next After the United Technologies Rockwell Collins Merger

The magnitude of the United Technologies Rockwell Collins merger ensures that the aftershocks will reverberate across the aerospace industry. For one, additional consolidation seems inevitable as scale becomes a critical enabler of cost-competitiveness. And as supply contracts become more onerous, relationships across all echelons of the supply chain will be tested, and many smaller players will face increasingly difficult strategic decisions.

UTC

After a half decade of acquisitions that brought Goodrich, B/E Aerospace, and Rockwell Collins product lines into the UTC family, the company will clearly devote its near-term efforts to integrating its new assets to form Collins Aerospace Systems. While UTC’s Otis and Climate, Controls and Security (CCS) segments look increasingly like outliers in this new aerospace-dominant conglomerate, ongoing R&D investment and healthy margins in Otis and CCS suggest that divestitures may not currently be in the company’s overall financial interest.

Prospects for additional aerospace acquisitions, meanwhile, are unlikely to match the stature of UTC’s most recent deal, as the market opportunity for additional presence aboard aerospace platforms is increasingly limited (and affected by antitrust concerns). Nevertheless, it would not be surprising to see UTC invest in smaller, accretive bolt-on solutions (e.g., adjacent electromechanical capabilities), vertical integration (e.g., electrical wiring and power systems), or in other aftermarket areas like the growing Parts Manufacturer Approval (PMA) domain, which is an emerging threat in some of UTC’s core segments (e.g., engines, electrical systems).

Aircraft OEMs

Aircraft OEMs

Although aircraft OEMs are continuously exploring ways to increase their leverage—such as dual- and sometimes triple-sourcing key components—Boeing, Airbus, Bombardier and Embraer can do little in the near-term to thwart the rise of a super-supplier.

With new narrowbody programs now entering service (e.g., Boeing 737MAX, Airbus A320neo, Bombardier CSeries), widebody aircraft delivery rates increasing (e.g., Boeing 787, Airbus A350), and next-generation platforms due to arrive by 2020 (e.g., Boeing 777X, Embraer E-Jet E2), picking fights with critical suppliers would be a highly risky endeavor.

Instead, battles between aircraft OEMs and their suppliers will likely not fully materialize until new aircraft programs are launched at the turn of the decade.

In assessing these future opportunities, aircraft OEMs have several responses to industry consolidation: they can reduce pressure on their component providers, find alternate sources, or stay the course, despite being inconvenienced by increasingly conglomerated suppliers.

The first option is a non-starter: it needlessly cedes hard-won concessions and significant aftermarket opportunity.

Turning to UTC’s competitors would send a strong message to others considering acquisitions, but would reduce effective competition and rob aircraft OEMs of expertise and quality, ultimately creating a narrow path to thread between risk and cost.

While Boeing’s willingness to enlist Héroux-Devtek for 777X landing gear illustrates a sizable degree of risk tolerance, prior developmental challenges on the 787 program will force it and other OEMs to carefully evaluate any additional supply base overhauls.

Due to the clear drawbacks of the first two options, aircraft OEMs will likely continue their current course of price concessions and contract renegotiations that enhance their aftermarket position.

The threat of additional insourcing will also likely become a mechanism to further pressure the supply base. In addition, Boeing and Airbus may seek to leverage their substantial lobbying power to prevent further supplier consolidation, arguing against the creation of quasi-monopolies.

As evidenced by Boeing’s aggressive stance in its current trade dispute with Bombardier, Boeing appears willing to leverage its political clout, and is likely emboldened by the substantial domestic labor force that it employs in today’s ‘Jobs First’ political environment.

In sum, through shrewd deployment of business, political, and regulatory tactics, OEMs will continue to “partner for success,” their march toward higher margins slowed but not stopped by a new breed of suppliers.

Other Tier 1 Providers

Tier 1 suppliers, especially UTC’s direct competitors, will likely find their financial futures increasingly impacted by UTC’s future reactions to aircraft OEM price demands. Should UTC acquiesce to some degree as the acquisition’s cost synergies materialize, near-peer suppliers will struggle to profitably compete.

Alternatively, if UTC uses its newfound leverage to try and preserve its margins, it may open the door for competitors to market themselves as a cheaper alternative.

Regardless, near-peer Tier 1 suppliers are undoubtedly already evaluating their own acquisition strategies, which will further reshape the composition of the supply chain.

Large players must keenly evaluate what is core to their portfolio and identify how they can maintain profitable access to both original production and aftermarket work.

For instance, GE Aviation is likely inclined to pursue future additions to counter UTC, given their direct competition in electrical power systems as well as Boeing’s move into avionics—a market area that GE itself entered through its 2007 acquisition of Smiths Aerospace.

Honeywell, Esterline, Moog, Parker Aerospace, Meggitt, and others will face a similar crossroads: remain on their current trajectory by caving to price concessions, but become a “trusted partner” to OEMs; acquire in order to remain cost-competitive with UTC as another “super supplier”; or hoist a “For Sale” sign to capitalize on what may increasingly become a seller-friendly market.

M&A is a logical outcome for many, yet it is not a sure-fire panacea: if companies grow too large and diverse, operations could become unwieldy and impede any potential integration benefits.

Furthermore, suppliers may face anti-trust headwinds with aggressive acquisition (though the strength of regulatory resistance will depend on whether the US and EU would seek to preserve effective global competition, or instead defend their respective aerospace regional champions).

Alternatively, should suppliers remain too small, they will likely lack the synergies, cost-competitiveness, and leverage that larger firms like UTC can now wield in almost every market segment.

Tier 2/3 Component Suppliers

As OEMs and Tier 1s grapple for leverage, perhaps the most profound implications of continued consolidation will trickle down to the lower echelons of the supply chain. Increasing clout among Tier 1 players in a zero-sum market necessitates a corresponding reduction in pricing power and aftermarket access for lower-level providers.

For these smaller firms, the coming decade will bring steadily intensifying pressure from customers to cut costs and cede IP rights – if they haven’t done so already.

Effectively countering such threats will depend on a myriad of factors, including the size of the supplier, its core capabilities, and its portfolio composition. In general, Tier 2 and Tier 3 providers, should look to find compelling merger opportunities or make internal investments that allow them to climb the value chain and provide more integrated systems that enable easier access to the aftermarket.

Navigating the Future

![]()

The United Technologies Rockwell Collins merger will inevitably act as a catalyst for continued repositioning and strategic adjustments across the aerospace supply chain. Regardless of size, positioning, or offerings, suppliers must ensure that long-term strategies are in place that address the following questions:

- How do we articulate a path to preserve pricing and platform positioning?

- How do we maintain relationships with key customers?

- What actions should be taken to ensure our own suppliers are held accountable while minimizing disruptions?

- How realistic is it to expect growth or a sustained presence in the aftermarket?

- What adjacent growth avenues exist that can counteract upcoming headwinds in our core portfolio?

- Should we be buyers or sellers in an active market, and what actions should we take to position as such?

A supplier that fails to map a clear strategic vision to navigate the path ahead runs the risk of finding itself adrift during a time of historic change.