South America’s Response to COVID-19 and the Defense Sector Impact

Despite South America’s response to COVID-19 the efforts to prevent the physical and economic effects of the crisis have been significant.

South America has seen varying responses to the COVID-19 crisis. Like many countries in other regions, South American nations have turned to their armed forces to both enforce lockdown measures and provide public health assistance during the crisis.

At the same time, local defense suppliers have been manufacturing medical equipment, ranging from ventilators to hospital beds.

Maintaining social distancing measures comes with a significant cost, both in terms of their economic impact and the need to fund significant military mobilizations.

Such effects serve to scupper attempts by some countries, such as Brazil, to generate economic growth following prior economic slowdowns. Whilst for countries such as Argentina, already struggling economically prior to the crisis, the effects could be disastrous.

This paper will examine South America’s response to COVID-19. Specifically:

- The current steps being taken by armed forces and defense suppliers in the region during the COVID-19 crisis;

- The economic impact of the current situation and the economic measures being taken in order to minimize the impact; and

- Finally, what implications all of this has for future defense spending.

Current Situation

Before exploring both the economic impact and effects on defense spending, it is necessary to outline the current situation regarding COVID-19 and South America’s response to COVID-19.

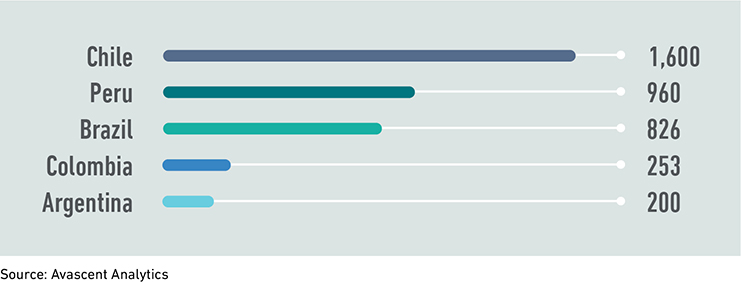

A number of South American countries have seen high rates of COVID-19 infection. Chile, Peru, and Brazil are in the top 12 countries, in terms of reported cases per share of the 2020 population.

Brazil

As of 10 July, there were 1,755,779 confirmed COVID-19 cases in Brazil, with 69,184 deaths.[1] The first case was confirmed on 25 February 2020, with the first death due to the disease announced on 17 March, when there had been 291 confirmed cases.

This led Santa Catarina to be the first state to declare a State of Emergency, closing non-essential businesses and suspending public transportation and gatherings.

This was followed by further social distancing measures at the State level across the country, including the announcement of a state-wide quarantine by Sao Paulo. Such measures are causing political friction in the country, with President Bolsonaro opposing a lockdown due to a desire to get businesses back up and running as soon as possible.

Bolsonaro has argued that the lockdown is doing more damage than the pandemic itself. However, with cases and deaths from COVID-19 continuing to rise it is difficult to see how preventative measures can be ended in the near future.

Peru

In Peru, there have been 316,448 confirmed cases and 11,314 deaths. The first case in Peru was reported on 6 March and the country has acted relatively quickly in order to prevent the spread of the virus, with President Vizcarra imposing a country-wide lockdown from 16 March.

Measures introduced include a curfew from 8 pm until 5 am, later extended to begin at either 6 pm or 4 pm in certain parts of the country.

Despite introducing what were seen as region-leading measures, when cases are examined in terms of prevalence rate per 100,000 of population the situation in Peru is worse than neighboring Brazil. This is due to the fact that despite the lockdown, much of the population relies on informal employment and had little option but to continue to work.[2]

Columbia

In Colombia, there have been 128,638 confirmed cases with 4,791 deaths.

The first case in the country was reported on 6 March with a State of Emergency being declared by President Duque on 17 March.

This was followed by a nationwide quarantine being announced on 21 March. This quarantine remains in force, however, there has been some easing in order to enable industrial sectors such as construction and manufacturing to restart.

Chile

In Chile, there have been 306,216 confirmed cases with 6,682 deaths.

The first case in the country was reported on 3 March. The first death in the country was reported on 21 March, leading to a nationwide nighttime curfew being introduced from 22 March.

This was followed by a series of lockdowns being established in various parts of the country from 26 March.

In order to keep its economy moving Chile has attempted to implement dynamic lockdowns, with quarantines being imposed and lifted strategically across the country.

A further sign that Chile wanted to keep as much of its economy open as possible could be seen in April when Chile announced a plan to introduced immunity passports for those already infected with the virus, however, this scheme was postponed in May.

The fact that the number of cases per 100,000 population is significantly higher in Chile compared to the rest of the region provides evidence that this dynamic approach was unsuccessful.

Argentina

Argentina also reported its first case on 3 March and as of 10 July, there have been 90,693 confirmed cases and 1,720 deaths.

The first death from the virus was reported on 7 March, the first in the region, with a nation-wide lockdown established from 20 March.

Figure 1: Confirmed COVID-19 Cases per 100,000 Population (10 July 2020)

South America’s Armed Forces and Defense Sector Response to COVID-19

Whilst South America’s response to COVID-19 has varied in terms of the time and scale of lockdowns, a common factor is that the armed forces in each country have been mobilized to provide assistance.

For some countries, this level of deployment is unprecedented in recent times.

Argentina, for example, has deployed 22,000 personnel, with Defense Minister Augustin Rossie stating that this is Argentina’s largest deployment of personnel since the Malvinas/Falklands conflict of 1982.

Such deployments are likely to have an impact on defense spending, with Operations & Maintenance and Personnel spending increasing.

There are indications that governments have recognized the potential squeeze on already pressed defense budgets, with Peru and Argentina both increasing defense spending for 2020 to support current deployments.

Peru has allocated an additional PEN108.6 million (USD32.0 million) to its O&M budget, of which PEN62.5 million (USD18.4 million) has been allocated to the army.

Argentina has raised defense spending by ARS500 million (USD7.45 million) whilst also providing each active member of the armed forces and police with an additional ARS500,000 payment in April 2020.

The need for such increases in O&M accounts is unsurprising given the fact that Personnel spending comprises approximately 70 percent of defense spending, leaving limited funds for operations.

the defense sector have been utilized during

the COVID-19 crisis, there is a significant

prospect that economic uncertainty will lead

to reduced defense spending in the near-term."

In addition to the armed forces, defense companies in the region have been playing an active role in South America’s response to COVID-19 by addressing the pandemic by producing medical equipment.

In Brazil, the Ministry of Defense has been working to identify companies that can provide medical equipment. By the end of April, approximately 240 companies had registered an interest with 470 separate products identified. These range from ventilators to face masks.[3]

In Chile, FAMAE and ENAER have partnered to design and produce a new ventilator under project Neyun.[4] At the same time shipbuilder, ASMAR has teamed with the University of Concepcion to produce similar ventilatory assistance equipment.

Economic Impact

Despite the fact that both the armed forces and the defense sector have been utilized during the COVID-19 crisis, there is a significant prospect that economic uncertainty will lead to reduced defense spending in the near-term.

Going into 2020 the economic situation for many of the countries in South America was far from prosperous.

Brazil

Still emerging from a recession in 2014-15, Brazil has experienced low levels of GDP growth in recent years. After a GDP growth rate of 1.3 percent in 2017 and 2018, 2019 saw this rate fall to 1.1 prompting fears the economy was once again heading towards a recession.[5]

The economic impact of COVID-19 has been significant. The fact that industrial output fell by 9.1 percent from February to March 2020 makes it highly likely that Brazil will enter a recession. Rather than if there will be a recession the question is now how deep will this recession be?

In April 2020 the International Monetary Fund (IMF) stated that it expected Brazil’s GDP to decline by 5.3 percent in 2020 before increasing by 2.3 percent in 2021.

Even if such a bounceback did occur in 2021, GDP that year would still be significantly lower than expected before the COVID-19 outbreak.

On 29 May it was reported that Brazil’s GDP contracted by 1.5 percent in the first quarter of 2020, with 4.9 million people losing their jobs in the three months from February through April.[2] This has led to suggestions that the overall fall in GDP for the year may, in fact, be higher than the 5.3 percent forecast by the IMF.

For example, in May Goldman Sachs revised its economic outlook for Brazil to forecast a 7.4 percent decline in GDP for 2020.[6] This contrasts with the 1.5 percent growth forecast by Goldman Sachs at the beginning of March 2020.[7]

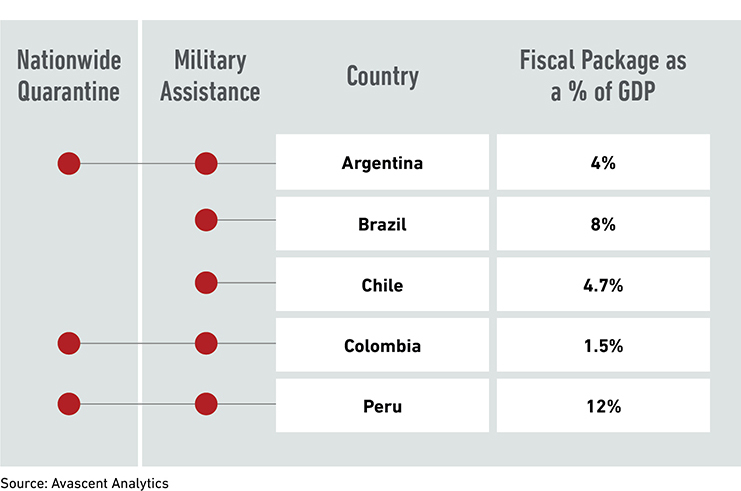

Brazil’s response to the economic effects of COVID-19 has involved a fiscal package worth 8 percent of GDP. These measures have included income support for vulnerable families as well as the extension of credit lines for businesses.[8]

Chile

Chile is currently feeling the effects of falling copper prices, which have dropped by 22.99 percent in 2020.[9]

At the same time, the country is emerging from a period of domestic instability, with violent protests in October 2019 causing a decline in the value of the Peso.

Whilst these protests have largely subsided due to COVID-19 and the subsequent lockdown, the potential for them to flare up again is clear. Discontent amongst the population remains, demonstrated by a protest on 21 April 2020.[10]

The risk for Chile is that further protests will hamper efforts to recover once lockdown measures are eased.

Chile has taken quick action in order to support its economy, announcing a fiscal support package worth USD11.75 Billion on 19 March 2020.[11] This equates to 4.7 percent of GDP.

These measures include higher healthcare spending, enhanced subsidies and unemployment benefits, and tax deferrals. A further USD 2 Billion was announced on 8 April to support the vulnerable and self-employed.

Efforts were taken to maintain copper output in Chile, however a failure to contain the virus has led to the slow down in operations in June 2020 in order to protect miners.

Argentina the hardest, largely due to the fact that

the economy was already in significant difficulty

before the outbreak."

Columbia

Colombia is expected to fare better than its regional neighbors due to the strength of its economy in 2019, with GDP growth at 3.3 percent.

Despite this relative strength a recession is still expected, with the IMF forecasting a contraction in GDP of 2.4 percent from 2019. However, based on the strength of 2019 demand, the IMF expects a higher rate of growth in 2021, with a 3.7 percent growth. Growth is then expected to remain at this level at around 3.5 percent.

Colombia’s response has been to establish the National Emergency Mitigation Fund. The fund, announced on 21 March, provides approximately USD3.7 Billion (1.5 percent of GDP).

Peru

With falling export demand, Peru is expected to see a drop in GDP of 4.5 percent in 2020, however, its bounceback in 2021 is expected to be significant at 5.3 percent.

Part of the reason for this is the fact that Peru has been able to provide the largest economic stimulus package in the region, at 12 percent of GDP.[12] PEN 25 billion (USD 7.27 billion) is being injected into the economy by finance minister Maria Antonieta Alva.

As one of the world’s largest food exporters, Peru is also in a strong position to meet global demand once it increases towards the end of 2020.

Argentina

Economically the COVID-19 crisis is expected to hit Argentina the hardest, largely due to the fact that the economy was already in significant difficulty before the outbreak.

Argentina was in a recession as of 2019 with GDP falling by 2.2 percent.

This contraction is expected to continue in 2020 and now be exacerbated further by the measures being taken to contain the virus. Therefore, the IMF is forecasting a decline of 5.7 percent in 2020.

Argentina’s situation is made worse by the fact that its public debt of USD323 billion is currently unaffordable. Despite efforts to restructure a debt of USD65 Billion with private bond holders, Argentina fell into default on 23 May for the 9th time in its history.

In doing so the country became the second country, after Lebanon, to default during the COVID-19 crisis. Negotiations on a long-term solution have continued with the deadline extended until late July, with indications that an agreement will eventually be reached. [13]

Despite this fact, the Government has been able to announce fiscal measures worth 4 percent of GDP. These measures include increased health spending, additional support to workers and vulnerable families, and support for the hardest hit industrial sectors.

Reduced Defense Spending?

With the COVID-19 outbreak causing economic crisis is many countries in South America, whilst at the same time exacerbating existing weakness in others, it is likely that future defense spending will decline as a result.

However, the exact nature of these cuts is difficult to determine. With so much of defense spending being absorbed by personnel budgets, it is difficult for South American countries to enact significant cuts without reducing end strength.

Security threats in the region, such as the Venezuelan refugee crisis, often require significant boots on the ground over investment in equipment. Reductions in end strength would also prove highly unpopular at a time of high and rising unemployment.

It is therefore likely that any budget cuts taken will fall most heavily on investment spending. This too is nuanced due to the fact that procurement funding is also used as a stimulus for local industry. This is particularly the case for shipbuilding.

Peru and Colombia are expected to recover relatively well from the current crisis, and it is, therefore, possible that significant defense cuts can be avoided. For Argentina, on the other hand, it is difficult to see a scenario where cuts are not made, especially if a debt restructuring plan cannot be found.

Brazil has so far managed to shield defense from any significant cuts, with President Bolsonaro reluctant to slash spending.

However, with the economy due to the contract, a reduction in defense spending now appears to be inevitable.

The fact that Chile’s defense investment is largely funded by the Copper Law, has traditionally protected procurement spending. Under current legislation, 10 percent of Codelco’s export revenue is allocated to defense procurement.

If there is an extended global downturn in industrial production as a result of a COVID-19 induced recession this could have a negative impact on the copper process due to reduced demand. With plans to replace the Copper Law with direct funding from government delayed, any fall in copper value would have a direct impact on defense spending.

Wider impacts for defense companies

Whilst any decline in defense spending will not affect local industry immediately, defense industries in the region have already started to feel the effects of the global crisis despite South America’s response to COVID-19.

Attendance at global trade shows has been affected due to the cancellation of the majority of events. At the same time, major exhibitions in the region have also been cancelled, affecting the ability of suppliers to run effective marketing campaigns. Cancelled events include the FIDAE Air and Space exhibition in Chile.

Perhaps the biggest immediate consequence of the COVID-19 crisis on South America’s aerospace and defense sector has been the fact that Boeing has withdrawn from its proposed joint venture with Embraer.

Such a merger would have provided a significant boost for the Brazilian company, particularly in providing further opportunities for its C-390 Millenium transport aircraft.

At a time when the commercial aerospace sector is being hit by a fall in demand, Embraer must now reevaluate its position in the market.

Despite the impact of COVID-19, production of the C-390 appears to continue unabated with delivery of the third KC-390, capable of air-to-air refueling, being made to the Brazilian Air Force in June 2020.

Announcing this delivery, Embraer pointed to the fact that the first two aircraft have been used extensively in support of the response to COVID-19.

Such a programme is important to Brazil, both in terms of economic benefit but also prestige. For this reason, it is unlikely that President Bolsonaro will be willing to let production slip.

However the same cannot be said for potential export orders and with a potential softening of the market in the coming years due to likely budget cuts, the fact that Embraer’s joint venture with Boeing did not come to fruition will still be a concern.

One advantage Brazilian aerospace companies do have is that previously contracted work is now beginning to flow through to the country.

This is particularly the case with the Gripen programme, with local production starting in July 2020 as a result of the technology transfer terms mandated in the contract. Of the 36 aircraft ordered, 15 are to be produced locally.

This provides local employment and expertise through Saab’s local subsidiary, Saab Aeronáutica Montagens, which is producing elements of the main body of the aircraft such as the front fuselage and tail cone.

Embraer is also a beneficiary of this work, providing final assembly at its facility in Sao Paulo.[14]

Significant Impact Despite South America’s Response to COVID-19

For the most part, South American countries have acted quickly and firmly in order to attempt to contain the spread of the COVID-19 virus.

Despite this, the crisis and the efforts to contain the spread of the virus have come at a high cost, both in terms of lives lost and economic damage.

Even where countries such as Argentina have been able to limit the number of fatalities, the prospect of a deeper recession is becoming a reality.

Sadly, Brazil, which has tried to balance controlling the disease with the economic damage, is likely to now suffer the double blow of a deep recession as well as an increased death toll.

For a region that was already struggling to emerge from previous downturns, this impact is significant.

Whilst the current COVID-19 crisis has seen increased utilization of the armed forces and in many cases, a short-term rise in O&M and personnel spending, the weak economic situation of many South American countries makes future spending cuts almost inevitable.

Footnotes:

[1] https://coronavirus.jhu.edu/map.html

[3] https://www.defesa.gov.br/noticias/68300-empresas-de-defesa-adequam-processos-e-desenvolvem-produtos-para-combate-a-covid-19

[4] https://www.defensa.com/chile/proyectos-respiradores-asmar-enaer-famae-seleccionados-entre-35

[6] Brazil’s first-quarter GDP falls 1.5% as Covid-19 cases climb, Andres Schipani, Financial Times, 29 May 2020

[8] https://riotimesonline.com/brazil-news/brazil/brazils-2020-gdp-likely-to-take-a-tumble-says-goldman-sachs/

[9] https://www.imf.org/en/Topics/imf-and-covid19/Policy-Responses-to-COVID-19#B

[10] World Economic Outlook, April 2020: The Great Lockdown, IMF, April 2020

[11] https://prensa.presidencia.cl/comunicado.aspx?id=148684

[13] https://www.nytimes.com/reuters/2020/06/03/world/americas/03reuters-argentina-debt-deal-analysis.html

[14] https://www.defensenews.com/global/the-americas/2020/07/07/brazil-starts-gripen-production/